How Consolidated Concepts Helps Optimize Indirect Spend Savings Across Locations

In the wake of rising food costs—up by more than 20%—and with 45% of restaurant operators cutting costs in other areas—managing indirect spend and savings effectively is crucial. Consolidated Concepts is here to help multi-unit restaurant operators optimize their indirect spend savings across all locations.

What is Indirect Spend?

Indirect spend encompasses the non-food and non-beverage expenses essential for restaurant operations. Categories include:

- Kitchen Supplies: Utensils, cookware, and appliances

- Tableware and Dining Supplies: Plates, cutlery, and napkins

- Cleaning and Maintenance: Cleaning products, pest control, and waste management

- Restaurant Supplies: Menu printing, packaging materials, and promotional items

- Utilities: Electricity, gas, and water

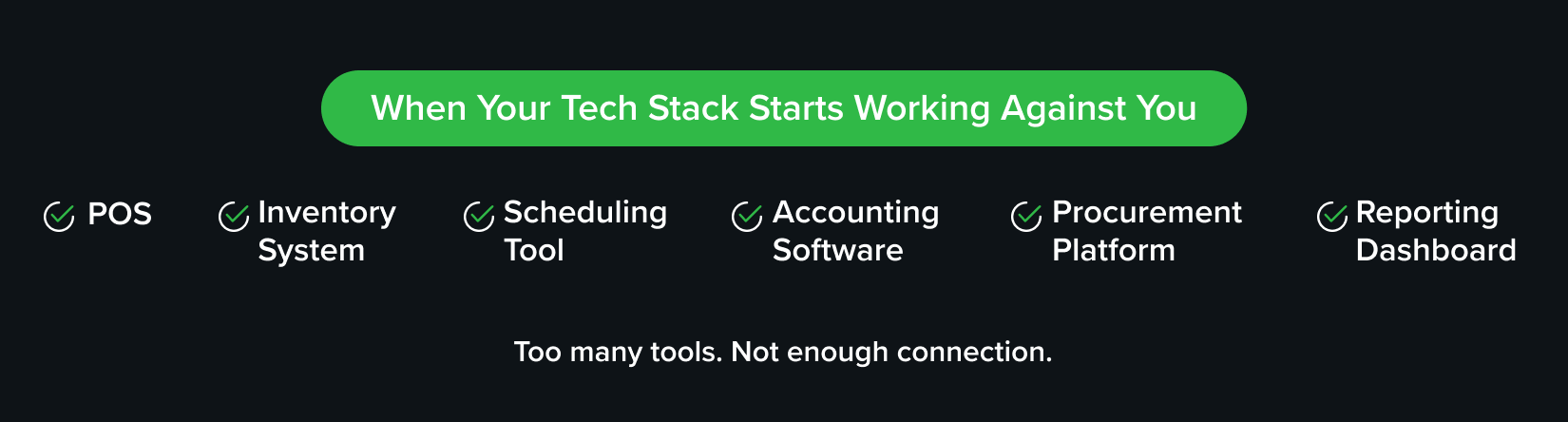

- Technology and IT Services: POS systems, software, and IT support

- Marketing and Advertising: Campaigns, online promotions, and printed materials

- Insurance and Legal Services: Liability insurance, permits, and legal consultations

How Do I Manage Indirect Spend?

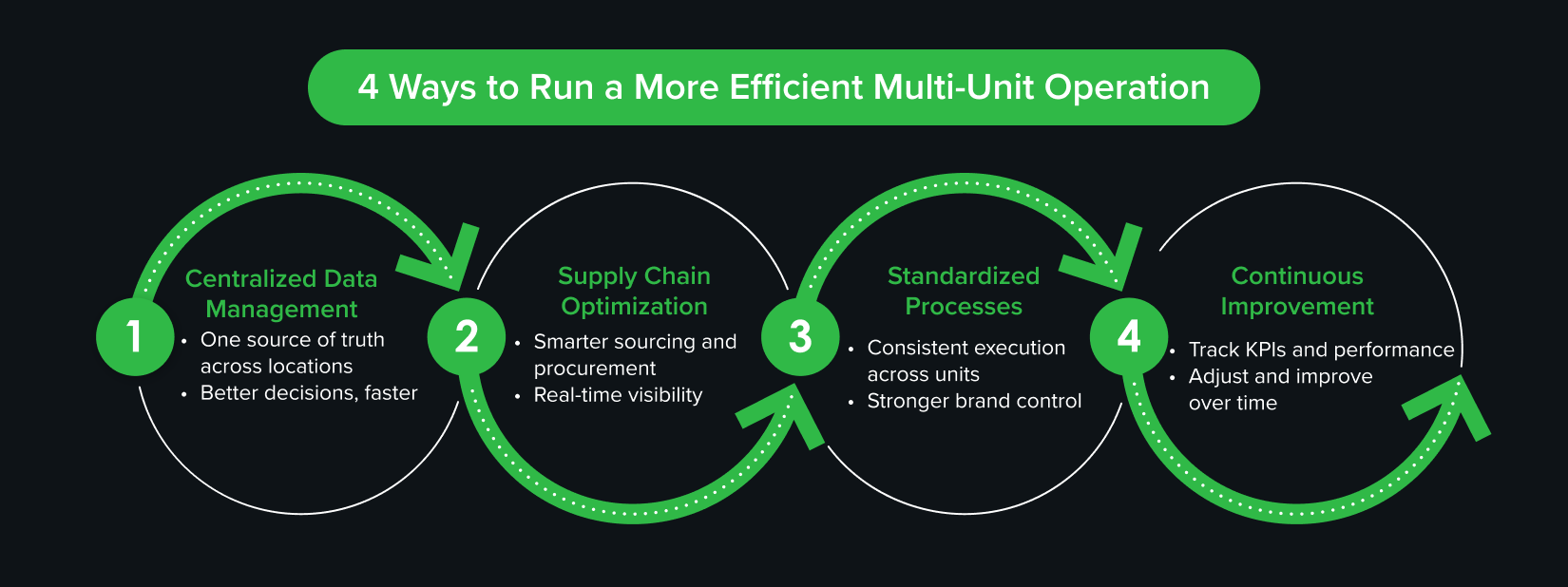

To effectively manage indirect spend across all locations, consider these 9 solutions that can streamline procurement, optimize spending, and enhance operational efficiency

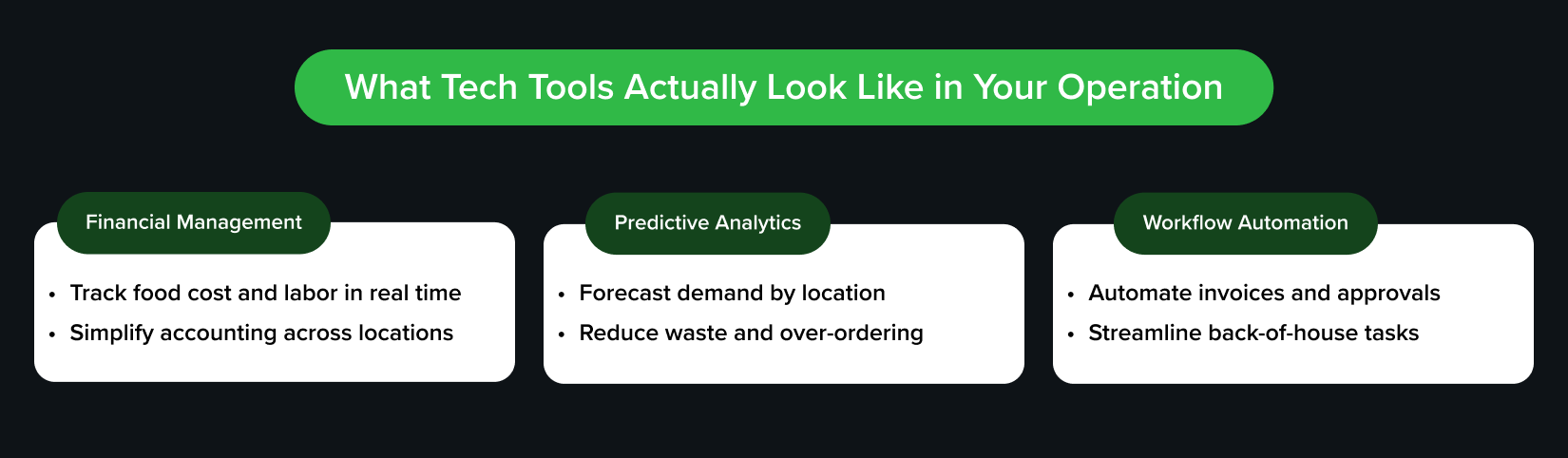

- Centralized E-Procurement Platforms: Streamline purchasing with a comprehensive platform, featuring automated ordering and electronic approval workflows.

- Advanced Spend Analysis Tools: Gain actionable insights into spending patterns and supplier performance to identify consolidation opportunities and negotiate better contracts.

- Efficient Supplier Management Systems: Maintain an organized supplier database, track performance, and manage contracts effectively to consolidate purchasing power and secure better pricing.

- Optimized Inventory Management: Automate tracking and control of indirect spend items to reduce waste, prevent stock issues, and enhance demand forecasting.

- Streamlined Digital Invoicing and Expense Management: Automate invoice processing and expense tracking to improve accuracy and provide real-time visibility into spending.

- Empowering Technology for Managers: Simplify ordering and management with technology that allows managers to place orders, monitor budgets, and track deliveries.

- Comprehensive Data Analytics and Reporting: Utilize data analytics tools to gain insights into spending trends and performance metrics, driving informed decision-making.

- Integration with Point-of-Sale Systems: Align procurement with sales data to optimize inventory levels and reduce excess stock or shortages.

- Continuous Improvement and Feedback: Adapt and refine processes based on feedback to continuously enhance efficiency and cost savings.

Leveraging solutions like these can help you manage and control indirect spend and maximize your indirect spend savings effectively across all your restaurant locations.

To learn more about the differences between direct and indirect spending, check out this article!

Maximize Indirect Spend Savings Across Locations

Front of House Savings

Consolidated Concepts helps you access exclusive discounts on:

- Uniforms: Cost-effective uniforms that enhance your brand image.

- Signage: Attractive signs that drive customer engagement.

- Television/Sports Packages: Entertainment options that enrich the guest experience.

- Payment Processing: Efficient systems that reduce transaction fees.

Back of House Savings

We offer big savings on:

- Sanitation: Effective cleaning solutions that maintain hygiene and reduce costs.

- Pest Control: Comprehensive programs that prevent infestations and maintain a clean environment.

- Waste Removal: Optimized waste management services that lower disposal costs.

- Utilities: Technologies that monitor and control utility usage for reduced bills.

Employee Benefits Programs

Consolidated Concepts supports retention with unique programs:

- Reward Programs: Tailored rewards to recognize and incentivize employees.

- Health and Wellness Benefits: Programs that support employee well-being and job satisfaction.

With food costs climbing and 18% of operators identifying them as their biggest challenge, optimizing indirect spend through technology is essential. By adopting e-procurement platforms, spend analysis tools, and efficient supplier management systems, multi-unit restaurant brands can achieve substantial savings and enhance operational efficiency.

Ready to maximize your indirect spend savings across all your locations? Partner with Consolidated Concepts and leverage our advanced technology solutions to streamline procurement, enhance operational efficiency, and drive significant cost reductions.

Fill out the form below to get started and discover how we can help you optimize your indirect spend and stay ahead in the competitive restaurant industry. Let’s work together to achieve substantial savings and elevate your operational performance!